Updated June 2026

What Is Uninsured Motorist Coverage Insurance?

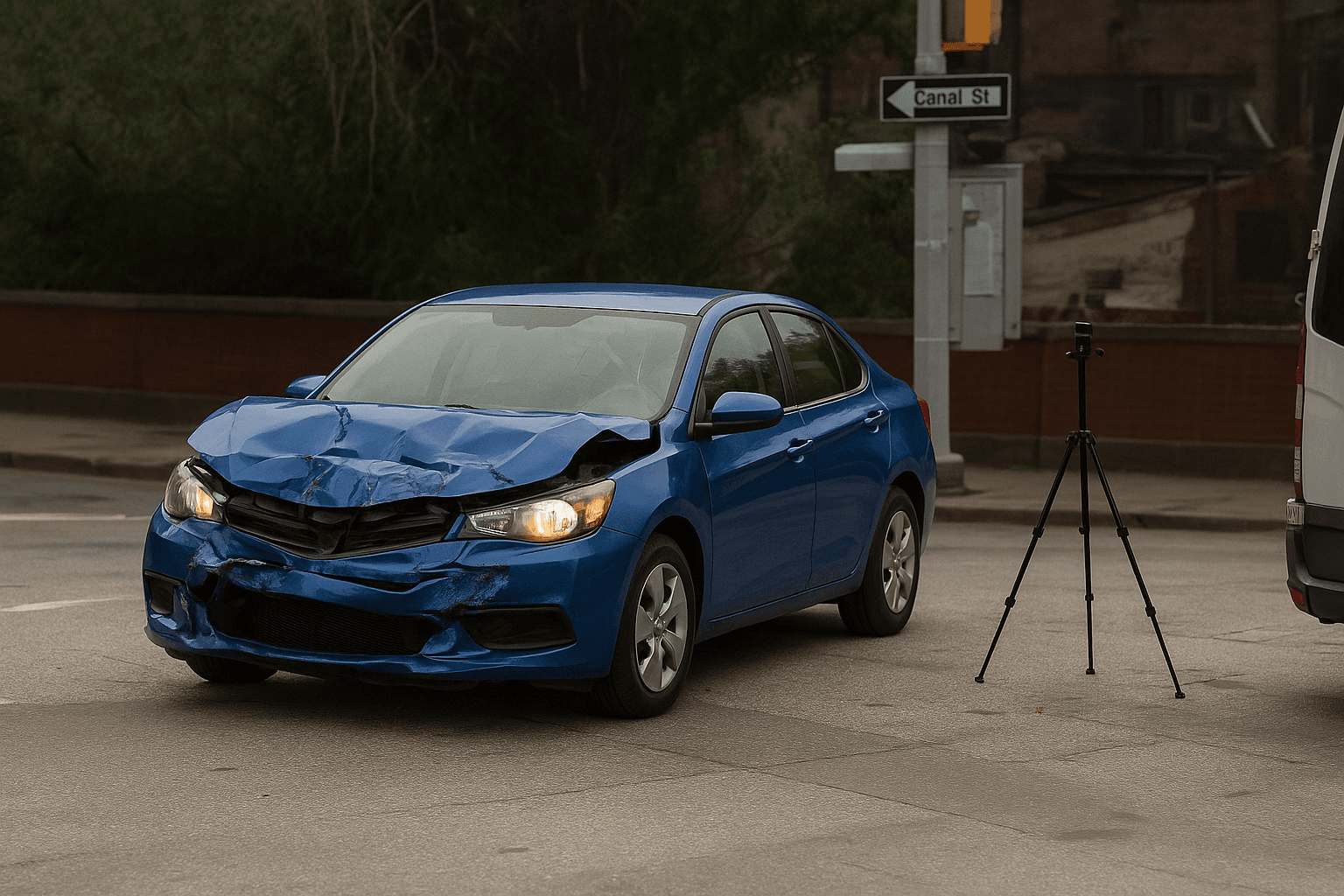

Uninsured motorist coverage (UM) is a policy add-on that pays for your medical expenses, lost wages, and vehicle damage when you're hit by a driver who has no insurance or insufficient coverage to pay your claim. It functions as backup protection when the at-fault driver can't cover what they owe you. South Carolina law requires carriers to offer UM coverage at limits matching your liability minimums, but you can reject it in writing—most suspended license holders skip it to keep reinstatement costs low, unaware that their SR-22 liability policy only covers damage they cause to others, not injuries or repairs they suffer.

- You're stopped at a red light and rear-ended by a driver with no insurance. You have $9,000 in medical bills and $4,500 in vehicle damage. The at-fault driver has no policy, so their liability coverage pays nothing. If you carry UM at $25,000/$50,000 with property damage, your UM coverage pays your $9,000 medical bill and $4,500 repair cost directly. Without UM, you pay out of pocket or sue the uninsured driver, who typically has no assets to collect against.

- A driver runs a stop sign and T-bones your car. You have $22,000 in medical expenses. The at-fault driver carries South Carolina's minimum $25,000 per person liability, which pays you the full $22,000. Your UM coverage doesn't activate because the other driver's liability fully covered your claim. UM only pays when the at-fault driver's limits are exhausted or nonexistent.

- Your parked car is sideswiped overnight and the driver flees. You have $3,200 in body damage. Standard UM property damage in South Carolina requires you identify the at-fault vehicle and driver—if you can't, UM won't pay. You'd need collision coverage to file this claim. Many drivers assume UM covers hit-and-runs; it typically does not unless the vehicle is identified.

Who Needs Uninsured Motorist Coverage Insurance?

UM makes sense if you're reinstating after suspension, don't own a vehicle outright, and can't afford to replace it or cover your own medical bills after an accident. South Carolina has one of the higher uninsured motorist rates in the Southeast—roughly 1 in 9 drivers—so the odds you'll eventually be hit by someone without coverage are material. If your SR-22 requirement lasts three years and you're driving daily to work, the cumulative exposure justifies the $100–$200 annual cost.

If your medical deductible plus vehicle replacement cost totals less than $5,000 and you have that amount in savings, rejecting UM to save $100–$150/year is defensible. If you're financing a car, have high-deductible health insurance, or lack emergency savings, the $10–$15/month UM cost is cheaper than the financial risk of being hit by an uninsured driver and covering everything yourself.

How Much Does Uninsured Motorist Coverage Insurance Cost?

UM coverage typically adds $8–$18 per month ($96–$216 annually) to a South Carolina policy at state minimum liability limits of $25,000/$50,000.

- Your liability limits—UM is offered at the same limits as your bodily injury liability, so higher liability limits raise UM cost proportionally.

- Whether you add UM property damage—covering vehicle repairs adds $3–$6/month on top of bodily injury UM.

- Your county's uninsured motorist rate—areas with higher percentages of uninsured drivers see slightly higher UM premiums due to claim frequency.

- Stacking election—if you insure multiple vehicles, stacked UM combines limits across all policies and costs 20–40% more than unstacked.

- Your driving record—suspended license holders reinstating with SR-22 pay higher base premiums, which increases the dollar cost of UM even though the percentage add stays consistent.