Updated June 2026

What Is Liability Insurance Insurance?

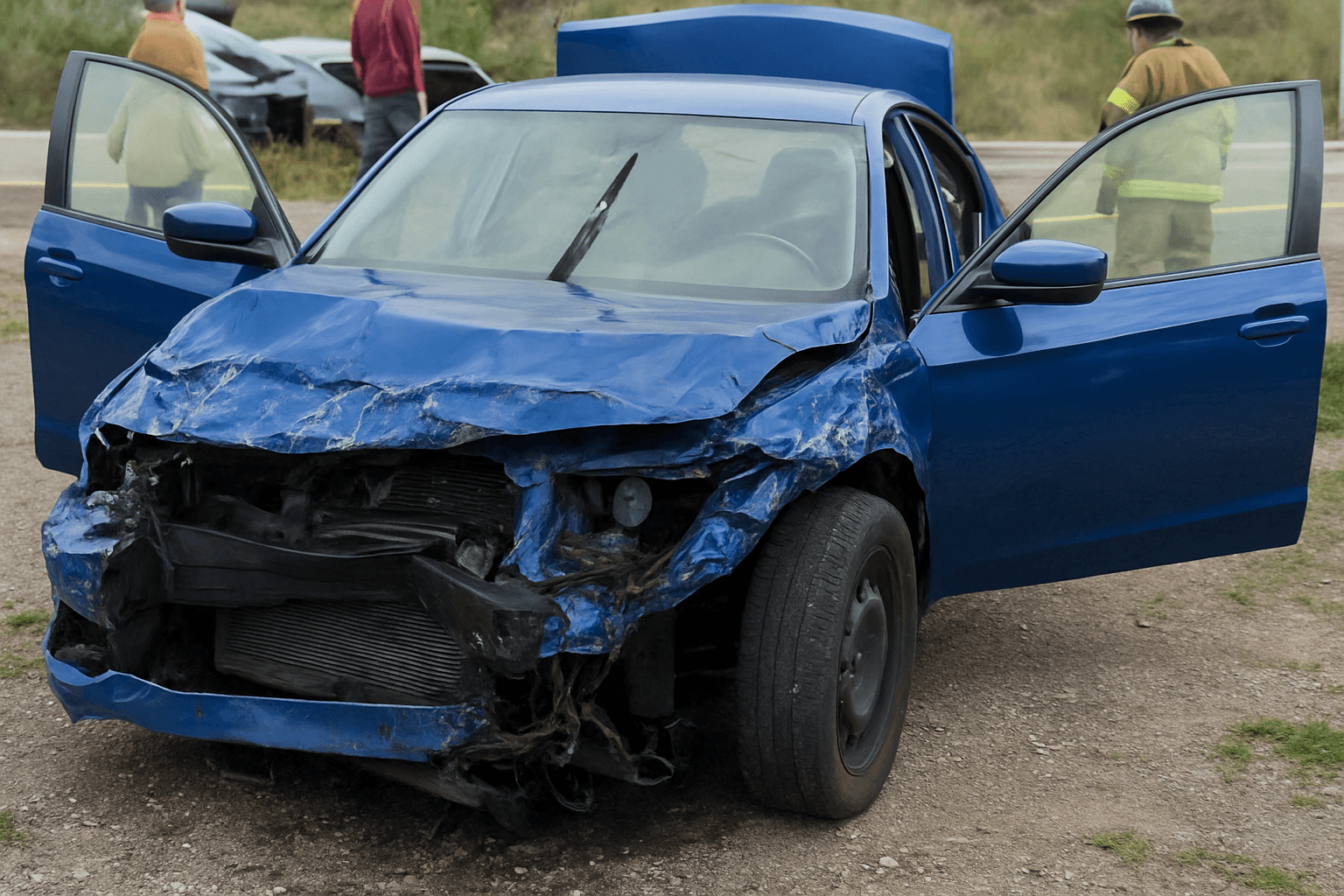

Liability insurance is a two-part coverage that pays when you cause an accident. Bodily injury liability covers medical bills, lost wages, and legal costs for people you injure. Property damage liability covers repair costs for vehicles, buildings, or other property you damage. Both coverages apply only to others — your own injuries and vehicle damage require separate collision and medical payments coverage.

- You rear-end a stopped vehicle at a red light. The other driver has $18,000 in medical bills and $6,500 in vehicle damage. Your 25/50/25 policy pays the full $18,000 in medical costs under bodily injury liability and the full $6,500 in vehicle damage under property damage liability. Your own vehicle damage is not covered — you pay that out of pocket or file a collision claim if you carry that coverage.

- You cause a three-car accident. Driver A has $30,000 in medical bills, Driver B has $22,000. Your 25/50/25 policy pays $25,000 to Driver A and $22,000 to Driver B — within the $50,000 per-accident bodily injury limit. Driver A can sue you personally for the remaining $5,000. Property damage claims from both vehicles total $32,000, but your property damage limit is $25,000 — you owe $7,000 out of pocket.

- You lose control and crash into a fence and mailbox on private property. Repair costs total $4,200. Your property damage liability pays the full amount. No bodily injury claim exists because no one was injured. If you also damaged your own vehicle, that repair cost is yours to pay unless you carry collision coverage.

Who Needs Liability Insurance Insurance?

You need liability insurance if your license is suspended and you are pursuing reinstatement in South Carolina — the state will not lift your suspension without proof of continuous coverage, even if you do not currently drive. You also need it if you own a vehicle during suspension, because South Carolina law requires liability coverage on all registered vehicles regardless of whether you have a valid license. If you are eligible for a route-restricted or hardship license, liability coverage at state minimums is the legal prerequisite before the DMV will issue the restricted credential.

Start with your suspension notice — if it lists SR-22 filing as a reinstatement condition, liability insurance is mandatory and you must maintain it for three years without lapse. If you own a vehicle, buy a standard liability policy on that vehicle. If you do not own a vehicle, buy a non-owner liability policy and request SR-22 filing from the carrier. If your suspension does not require SR-22, you can wait to buy coverage until 30 days before your reinstatement eligibility date, but continuous coverage from the suspension date forward will result in better rates and faster approval.

How Much Does Liability Insurance Insurance Cost?

Liability-only policies in South Carolina for SR-22 filers typically cost $95–$165/month ($1,140–$1,980/year) at state minimum 25/50/25 limits. Raising limits to 50/100/50 adds $25–$45/month.

- SR-22 filing status increases base liability rates 40–70% compared to standard drivers due to demonstrated high-risk history.

- At-fault accidents in the past three years add $30–$60/month to liability premiums, and multiple accidents can double your rate.

- DUI convictions raise liability costs more than other violations because they signal both risk and mandatory SR-22 filing requirements.

- County of residence affects pricing — Richland and Charleston counties show 15–25% higher liability rates than rural counties due to claim frequency.

- Credit-based insurance scores impact liability pricing in South Carolina; suspended license holders often see substandard credit tiers that increase premiums 20–50%.

- Continuous coverage gaps during suspension result in higher liability rates upon reinstatement — carriers view coverage lapses as additional risk indicators.